04 August, 2026

As the name implies, the triangulation simplification provisions set out in Council Directive 2006/112/EC (the “VAT Directive”), provide for the application of an exempt intra-Community acquisition in the country where the transport of goods ends. It is effectively a simplification which avoids a VAT registration for party B which makes an acquisition of goods followed by a domestic supply in the country where the transport ends. Subsequently, the VAT liability on the domestic supply taking place in that country, shifts onto party C.

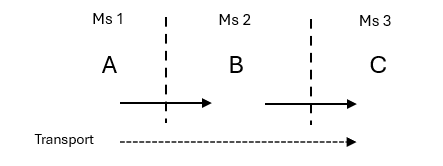

The triangulation simplification applies in the context of a chain transaction, specifically where three independent parties, A, B, and C, identified for VAT purposes in three different Member States transact with one another in a supply of goods between A and B, and B and C, with the goods being dispatched/transported from A’s Member State and ending in C’s Member State. As can be noted, a basic triangulation scenario entails two supplies with only one intra-community transport. In this article we will be surveying the pertinent VAT Directive provisions and how to apply them in practice as well as pointing out any pitfalls that may impact our conclusions.

As stated above, the triangulation simplification is applicable insofar as three separate taxable persons are identified for VAT in three different Member States, carry out two consecutive supplies with one cross-border transport. The transport, in the context of this tripartite transaction must be ascribed to one of the supplies and in order for the triangulation simplification to apply it must be ascribed to the first supply. As a result, the cross-border transport is carried out either by A, B or any person acting on their behalf (such as a logistics company). If the IC transport were to be carried out by party C, the simplification cannot be applied.

It follows that, Article 141 of the VAT Directive sets out the conditions that must be met for the simplification to apply. Let us examine the following typical scenario in the context of these conditions:

Under the triangulation simplification:

As already mentioned, the triangulation simplification is rendered inapplicable if the cross-border transport from the Member State of origin is carried by or on behalf of a third party. It is also to be ensured that at the point in time of the acquisition of the goods in the Member State of origin, the intermediary party already knows that he will be making a subsequent supply to the third party in the third Member State.

In conclusion, whilst the triangulation simplification and its application in practice may appear straightforward nevertheless some complications may arise where seeking expert advice, would be highly recommended.

[1] It is worth noting that some Member States do not allow the Article 141 exemption on the intra-Community acquisition by the middle party if the latter, notwithstanding not being established there, holds a VAT registration number in that Member State.

Author: Brandon Gatt, Partner, Zampa Partners

...

...

...

...

...

...

...

...