24 March, 2026

Key Highlights

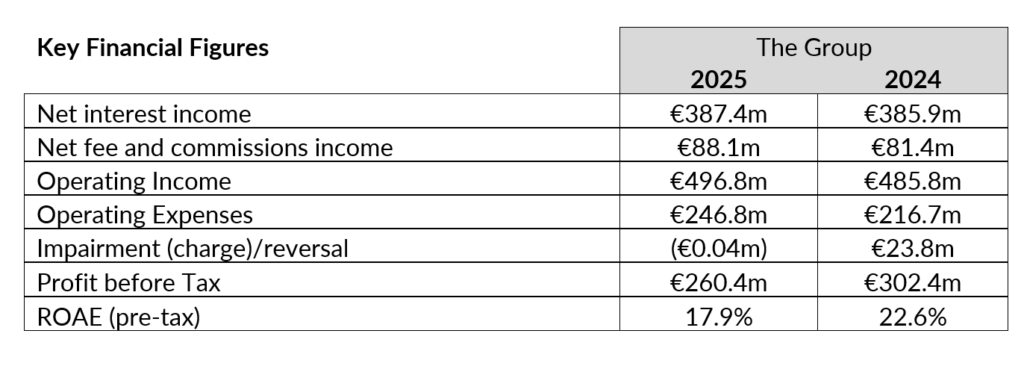

The Bank of Valletta Group delivered a solid performance in 2025, generating a Profit Before Tax of €260.4 million and achieving a pre‑tax Return on Average Equity of 17.9%. This outcome reflects the strength of the Group’s underlying business model, the resilience of its core income streams, and the disciplined execution of its strategic priorities throughout the year. The Group continued to improve its balance sheet, enhance asset quality, diversify revenues and invest in its operational and digital capabilities. As a result, it enters 2026 with stronger financial foundations and clear momentum for the next phase of its strategic development.

The strong financial performance enabled the Board to propose one of the most substantial dividend distributions in recent years, with a final gross cash dividend of €65.1 million (€42.3 million net) being recommended for approval from H2 profits, equivalent to €0.1014 per share gross (€0.0659 net). Over and above, the Board also proposed a special dividend of €10.4 million gross (€6.8 million net), equivalent to €0.0162 per share gross (€0.0105 net). This special distribution reflects the portion of profitability generated during the financial year that exceeded the upper bound of the Bank’s forward‑looking PBT guidance which amounted to €250 million.

This results in a total cash dividend for FY25 (including interim payment and special dividend) of €0.2032 gross (€0.1320 net) per share, and equivalent to a total gross dividend of €130.5 million (€84.8 million net) out of the year’s profits, with the payout being fully aligned with the Group’s Shareholder Distribution Policy. The distribution underscores the Board’s commitment to delivering sustainable shareholder returns while preserving the capital strength and strategic flexibility needed to support future growth.

Complementing this cash dividend, the Bank has also allocated a €7.8 million reserve during the year to operate the regulated share buyback programme, activated during FY2025. This contributed to improved equity liquidity and more efficient capital management, showing the ever-increasing trust that markets, shareholders and the wider community have in BOV.

During the year, the Group strengthening its long‑term funding through targeted capital‑markets activity, completing the issuance of €150 million in unsecured Tier 2 bonds, concluding the €250 million EMTN programme launched in prior year. The Bank subsequently obtained regulatory approval for a new €325 million programme, under which €125 million in unsecured subordinated (Tier 2) bonds were issued, further enhancing the capital structure and supporting future growth. In parallel, the Group has commenced engagement with international markets in preparation for a €300 million Senior Preferred issuance, aimed at broadening and diversifying its wholesale funding sources while ensuring continued alignment with evolving MREL and strategic funding requirements. Further details will be issued during FY2026, with the issuance being subject to regulatory approval.

Financial Performance and Prevailing Economic Conditions

Despite normalising interest rates and sector-wide cost pressures, the Group delivered a solid financial performance, exceeding profitability targets and forward-looking expectations. While profitability declined when compared to FY2024, core operating performance remained resilient, with operating income increasing by 2.3% year-on-year, supported by disciplined balance sheet management, credit portfolio expansion, non-funded income diversification, and active cost and impairment management.

The Group further strengthened its balance sheet, with total assets increasing by €1.4 billion, with year-end figures exceeding €16.5 billion. Expansion was driven by sustained growth in customer deposits, which increased by €937 million, together with a €277 million rise in long-term liabilities following the successful issuance of Tier 2 subordinated debt, supporting strong loan book performance and expansion of the investment portfolio beyond targets.

One of the most substantial dividend distributions in years – Dr Gordon Cordina, Chairperson

Speaking during the announcement of the Group Financial Results, Chairperson Dr Gordon Cordina, said that “The Bank delivered strong profits notwithstanding the significant geopolitical tensions abroad, the normalisation of interest rates, and upward pressures on operating expenses. This highlights the resilience of our business model, the prudence of our strategic decisions, and our commitment to sustainable performance and effective risk management. The Group’s performance for 2025, which exceeded the initial profit guidance, enabled us to declare one of the most substantial dividend distributions in recent years.”

Dr Cordina continued by stating that, “As the country’s largest bank, developments within the Maltese economy directly influence our performance, just as our actions have a significant impact on households and businesses. Against this backdrop, throughout 2026, we will shape our next three-year strategy, remaining mindful of the risks, opportunities, and responsibilities we carry as Malta’s leading financial services institution.”

Enhancing Customer Value, Accessibility, and Market Leadership – Kenneth Farrugia, CEO

CEO, Kenneth Farrugia, said that “During 2025, the BOV Group strengthened its leadership position across key customer segments, supported by targeted product innovation and improved customer experience. In retail business, home and personal lending, the Bank achieved double-digit growth. We strengthened our advisory capabilities, upgraded and modernised branches, opened a new Investment Centre in Sliema and upgraded two thirds of our ATM network. Our commercial banking performance also remained strong, with the relocation of our commercial operations to the Quad Central and a new Business Branch marking a strategic upgrade in service delivery. This reinforces our position as the Bank of Choice for both personal and commercial banking needs in Malta.”

Financial Performance

Operating income increased by 2.3% year-on-year, reflecting momentum across core business lines, optimisation of the funding and investment mix, and progress in revenue diversification. Commercial, Retail and Treasury remained the main pillars of income generation, delivering stable and recurring revenues.

Net Interest Income remained central to operating performance, increasing to €387.4 million as the Bank mitigates interest‑rate volatility through focused balance sheet optimisation and strong loan and investment activity. Net Fee and Commission Income also strengthened, rising by 8.2% to €88.1 million, driven by higher customer activity and the shift towards a more diversified, fee‑based earnings model.

Operating costs increased by 13.9% to €246.8 million over the prior year, reflecting a multi‑year investment programme aimed at strengthening technology, risk‑management and customer‑facing channels. Higher technology and cybersecurity expenditure mirrors accelerated digital implementation, transformation and resilience initiatives. Despite this, operating efficiency remains solid, with the cost‑to‑income ratio standing at 49.7% (FY2024: 44.6%).

The Non‑Performing Exposures ratio declined to 1.68%, supported by active remediation, improved portfolio monitoring and continued reduction of legacy positions. The coverage ratio increased to 59.4%, reflecting a resilient provisioning and approach to asset‑quality.

The Group’s profitability translated into a pre‑tax Return on Average Equity of 17.9%, comfortably above the 15% guidance. The year‑on‑year movement reflects both lower overall earnings when compared to the exceptional 2024 base and a higher average equity position driven by retained profits.

Profits from insurance associates increased to €10.4 million, reflecting the solid performance of the Group’s insurance operations in partnership with MAPFRE and their continued contribution to diversified earnings.

ESG remained a core priority, with progress on the Climate Transition Plan and further reductions in Scope 1 and Scope 2 emissions.

Outlook and Risk Management

The Group continues to monitor economic and geopolitical developments through risk monitoring frameworks, with assessments indicating no material emerging risks. Stress‑testing under ICAAP confirms strong capital buffers and resilience, while the Group remains vigilant towards maintaining transparent market disclosure.

The Board remains confident in the Group’s strategic direction, having delivered another year of strong performance underpinned by solid fundamentals, disciplined risk management and investment. Entering FY2026 from a position of strength, the Group remains focused on delivering sustainable growth, shareholder value and continued support for the Maltese economy.

...

...

...